- Home

- Investing

- Commodities

Profits from selling physical gold and silver, and even some precious metal funds, are taxed differently from other investments.

By

Sandra Block

published

25 March 2026

in Features

By

Sandra Block

published

25 March 2026

in Features

When you purchase through links on our site, we may earn an affiliate commission. Here’s how it works.

- Copy link

- X

Profit and prosper with the best of Kiplinger's advice on investing, taxes, retirement, personal finance and much more. Delivered daily. Enter your email in the box and click Sign Me Up.

Contact me with news and offers from other Future brands Receive email from us on behalf of our trusted partners or sponsors By submitting your information you agree to the Terms & Conditions and Privacy Policy and are aged 16 or over.You are now subscribed

Your newsletter sign-up was successful

Want to add more newsletters?

Delivered daily

Kiplinger Today

Profit and prosper with the best of Kiplinger's advice on investing, taxes, retirement, personal finance and much more delivered daily. Smart money moves start here.

Signup +

Sent five days a week

Kiplinger A Step Ahead

Get practical help to make better financial decisions in your everyday life, from spending to savings on top deals.

Signup +

Delivered daily

Kiplinger Closing Bell

Get today's biggest financial and investing headlines delivered to your inbox every day the U.S. stock market is open.

Signup +

Sent twice a week

Kiplinger Adviser Intel

Financial pros across the country share best practices and fresh tactics to preserve and grow your wealth.

Signup +

Delivered weekly

Kiplinger Tax Tips

Trim your federal and state tax bills with practical tax-planning and tax-cutting strategies.

Signup +

Sent twice a week

Kiplinger Retirement Tips

Your twice-a-week guide to planning and enjoying a financially secure and richly rewarding retirement

Signup +

Sent bimonthly.

Kiplinger Adviser Angle

Insights for advisers, wealth managers and other financial professionals.

Signup +

Sent twice a week

Kiplinger Investing Weekly

Your twice-a-week roundup of promising stocks, funds, companies and industries you should consider, ones you should avoid, and why.

Signup +

Sent weekly for six weeks

Kiplinger Invest for Retirement

Your step-by-step six-part series on how to invest for retirement, from devising a successful strategy to exactly which investments to choose.

Signup + An account already exists for this email address, please log in. Subscribe to our newsletter

Gold hasn't been this hot since prospectors rushed to California with picks and shovels to seek a fortune. Convinced that the runup will continue, investors have flocked to buy gold, which has never been easier.

You can buy gold bars at Costco or add exchange-traded funds that invest in physical gold to your retirement portfolio. And if you have gold jewelry or coins you no longer want, a “We Buy Cash for Gold” retailer will pay you a healthy sum for your shiny objects.

But whether you're buying or selling gold, it's important to understand how you'll be taxed on your profits. The IRS classifies gold — along with other precious metals — as a collectible, which means it's taxed at a higher rate than stocks, bonds and real estate.

Article continues belowFrom just $107.88 $24.99 for Kiplinger Personal Finance

Become a smarter, better informed investor. Subscribe from just $107.88 $24.99, plus get up to 4 Special Issues

CLICK FOR FREE ISSUE

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more - straight to your e-mail.

Profit and prosper with the best of expert advice - straight to your e-mail.

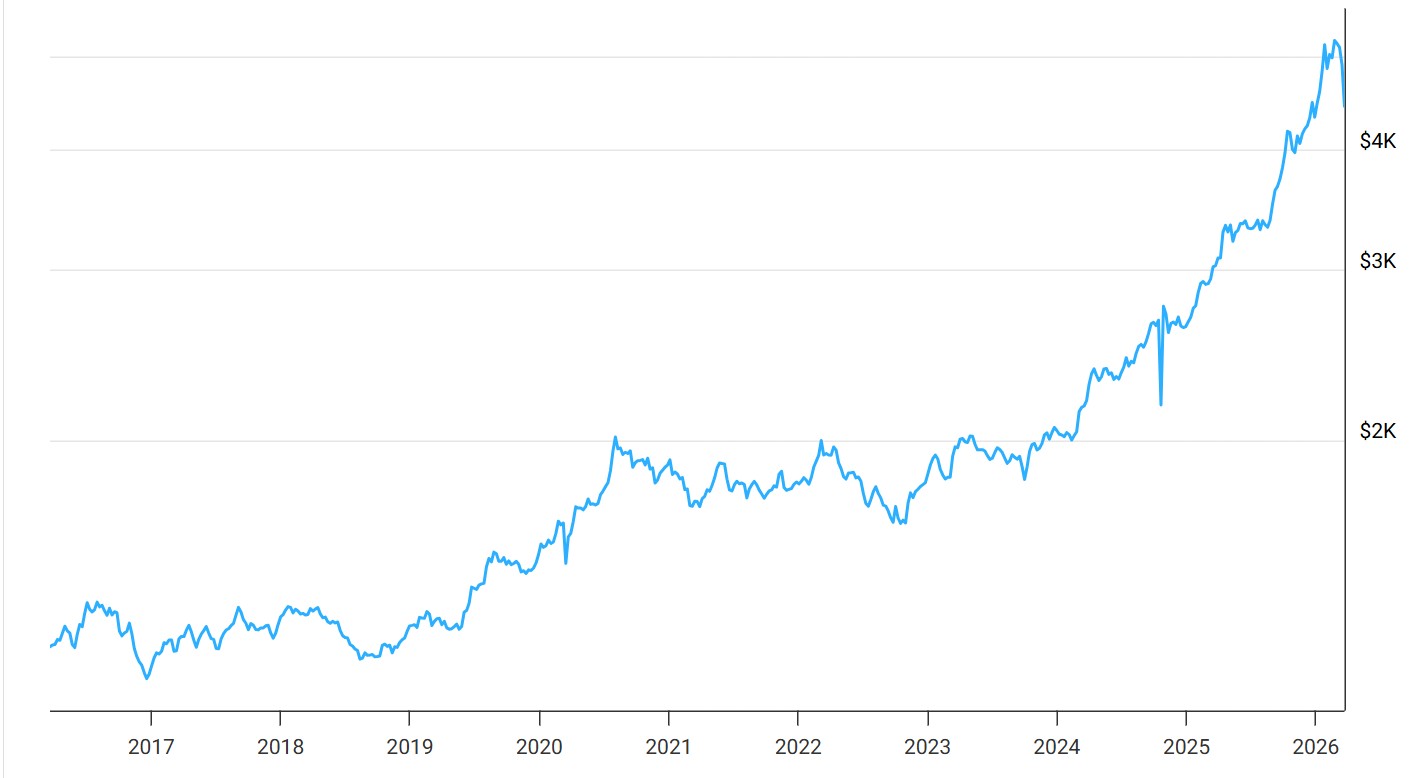

Sign upThe price of gold in U.S. dollars over the past 10 years

The top long-term tax rate for collectibles is 28%, versus 20% for long-term capital gains on securities. If you're subject to the 3.1% surtax on net investment income, which applies to taxpayers who have investment income and modified adjusted gross income of more than $200,000 ($250,000 for married filers who file jointly), you could pay up to 31.8% on your long-term gains.

As is the case with other investments, short-term gains on gold are taxed at your ordinary income tax rate.

Surprise! "Long-term gains from [ETFs] that are backed by physical gold are also subject to the tax rate for collectibles." — Marianela Collado

Rates on ETFs backed by precious metals vs mining companies

The higher rate isn't limited to gold bars and other physical assets. Long-term gains from exchange-traded funds that are backed by physical gold are also subject to the tax rate for collectibles, says Marianela Collado, a financial planner in Fort Lauderdale, Fla.

This often comes as a surprise to investors who assume their profits are taxed at the same rate as those from other ETFs, she says.

However, if you invest in a gold mining company or fund that invests in mining concerns, you'll pay the capital gains rate that applies to securities, says Mark Stancato, a planner in Decatur, Ga.

There are strategies you can use to soften the tax hit on your gold investments. Gold prices have been extremely volatile in recent months, and you can use that to your advantage.

If you bought a gold ETF during a recent runup and have since seen the price decline, you could sell shares and use the loss to offset some of your gains.

While investors who bought gold several years ago may not have any losses, “for people who got in more recently, volatility presents a great option for some tax loss harvesting,” says Mike Casey, a planner in McLean, Va.

Just be aware of the wash sale rule, Collado notes. If you sell an ETF (or other investment) at a loss and buy it back within 30 days before or after the sale, the loss isn't deductible.

Tax on sales of jewelry and other keepsakes

If you took advantage of the runup in gold prices to sell jewelry, gold coins or other items, the top 28% rate on collectibles applies to those profits, too.

Dealers are required to report sales of gold bars and coins to the IRS on Form 1099-B if certain conditions related to purity and quantity are met.

Even if the dealer doesn't file a 1099-B, the IRS expects you to report the sale on your tax return and pay taxes on the difference between the amount you paid for the items — known as the basis — and the amount you received in the sale.

If you received a gold item as a gift, the basis is the amount the donor paid for it; for inherited collectibles, the basis is the fair market value of the item on the date of the donor's death. Tracking down the basis is critical because otherwise, the entire amount of proceeds from the sale is considered taxable.

Dealers typically gauge the purity of items they buy and pay sellers the meltdown value, minus their own discount. But before you consign your grandfather's cufflinks to the furnace, make sure their intrinsic value doesn't exceed their scrap price, which could be the case if you own a vintage piece that was created by a sought-after designer. A jewelry appraiser can help you determine whether the item is worth more than the sum of its golden parts.

Note: This item first appeared in Kiplinger Retirement Report, our popular monthly periodical that covers key concerns of affluent older Americans who are retired or preparing for retirement. Subscribe for retirement advice that’s right on the money.

Read More

- What Is Your Collection Worth? How to Value and Protect Your Assets

- Should I Sell My Old Silverware and Gold Jewelry Now That Prices Are So High, or Should I Hand Them Down?

- Decluttering and Selling Your Stuff? What You Need to Know About Taxes

Sandra BlockSocial Links NavigationSenior Editor, Kiplinger Personal Finance

Sandra BlockSocial Links NavigationSenior Editor, Kiplinger Personal FinanceBlock joined Kiplinger in June 2012 from USA Today, where she was a reporter and personal finance columnist for more than 15 years. Prior to that, she worked for the Akron Beacon-Journal and Dow Jones Newswires. In 1993, she was a Knight-Bagehot fellow in economics and business journalism at the Columbia University Graduate School of Journalism. She has a BA in communications from Bethany College in Bethany, W.Va.